For serious Brisbane buyers who refuse to overpay!

When Dreams Become Nightmares: A 45-Year Journey Through Australian House Prices

I still remember the excitement of going with mum to look at a house that was nearly finished being built. It was going to be our first house. I was young then—too young to understand the significance of those numbers being discussed, but old enough to feel the anticipation in the air. All I knew was that we were getting our own place, and that felt like the biggest achievement in the world.

That house cost $42,000 in 1979. It seemed like an enormous sum of money at the time, and mum and her partner had to stretch to make it work.

Join the #1 Newsletter for Property People.

But it was achievable—a solid investment in our family's future that represented hope and possibility. Looking back now, I realize I witnessed something that may never happen again: a generation buying their first home at a price that actually made sense.

Recently, curiosity got the better of me, and I decided to look up that same house. Today, according to Real Estate .com it's worth $1.47 million. As an exercise, I thought I'd dig deeper into what these numbers actually mean—and what I discovered has me questioning everything we assume about the Australian housing market.

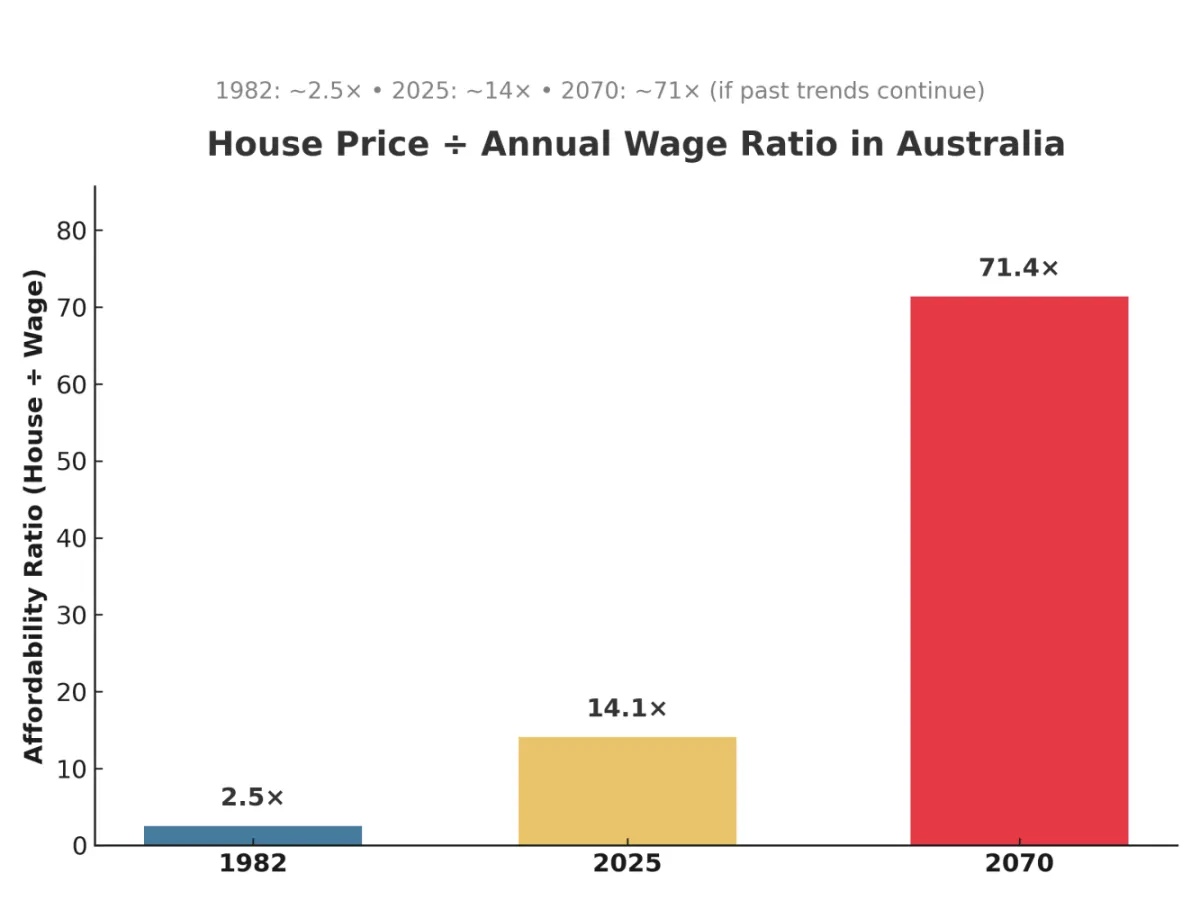

The Mathematics of Madness

So I got out my calculator and started crunching some numbers. Over those 45 years, that little house has increased in value by roughly 35 times. Not a bad return on investment, you might think. But then I asked myself a more unsettling question: what if this trend continues for another 45 years?

If house prices keep growing at the same rate they have since 1979, that $1.47 million house will be worth approximately $51.5 million by 2070.

Fifty-one and a half million dollars. For the same modest family home.

But here's where it gets really interesting. I decided to look at these prices not just in dollar terms, but in relation to what people actually earn. According to Australian Bureau of Statistics data, when mum bought that house in 1979, it cost about 2.5 times the average Australian wage. It was a stretch, but it was manageable for a working family.

Today, that same house at $1.47 million represents roughly 14 times the average Australian wage. Already, we've moved from "challenging but achievable" to "nearly impossible for most families."

But if we project forward to 2070, assuming both wages and house prices continue growing at their historical rates, that house would cost approximately 71.4 times the average wage.

Let that sink in for a moment.

The Impossibility of Forever

Seventy-one times the average wage for a basic family home. Even writing those words feels absurd.

Think about what this actually means in practical terms. If someone in 2070 wanted to buy that house and put down a 20% deposit, they'd need to save 14.3 times their entire annual salary—just for the deposit. The remaining mortgage would require payments that dwarf their total income, let alone leave anything for food, transport, or the small luxuries that make life worth living.

This isn't just mathematically challenging; it's mathematically impossible for the vast majority of people. Which raises an uncomfortable question: if we all accept that a 71-times wage multiple is ridiculous, at what point did we cross the line from "expensive but possible" to "fundamentally broken"?

Was it at 5 times the average wage? Ten times? Are we already living in that impossible future, just earlier in the timeline?

The more I stared at these numbers, the more I began to wonder whether we've been living through something extraordinary—a golden period of asset price growth that we've mistaken for normal. We've become so accustomed to annual house price increases that we treat them as a natural law, like gravity or the sunrise.

But what if they're not?

The Golden Period Delusion

Perhaps we've been living through an anomaly, not a new normal. The past 45 years have coincided with some pretty unique economic conditions: falling interest rates from historic highs, massive demographic shifts as baby boomers entered their peak earning years, financial deregulation that made credit more accessible, and a sustained period of economic growth that now seems almost quaint in its consistency.

These weren't permanent features of the economic landscape—they were temporary tailwinds that happened to align for nearly half a century. But tailwinds don't blow forever.

The question isn't really whether house prices can continue growing at 35 times over the next 45 years. The question is whether we're brave enough to admit that they can't, and what that means for how we think about property, wealth, and the Australian dream.

If a house costing 71 times the average wage sounds impossible, then something has to give. Either wages need to grow dramatically faster than they have historically, house prices need to grow much slower (or even fall), or we need to fundamentally rethink what homeownership means in this country.

The mathematics are simple. The implications are not.

So here's my question for you: when you look at these numbers, do you see the continuation of a trend, or do you see the end of an era? And if it's the latter, what comes next?

CUSTOMER CARE

LEGAL

FOLLOW US

Copyright THE OPPORTUNITY REPORT 2026. All Rights Reserved.