For serious Brisbane buyers who refuse to overpay!

Same Property. Three Prices. One Brutal Lesson About Timing.

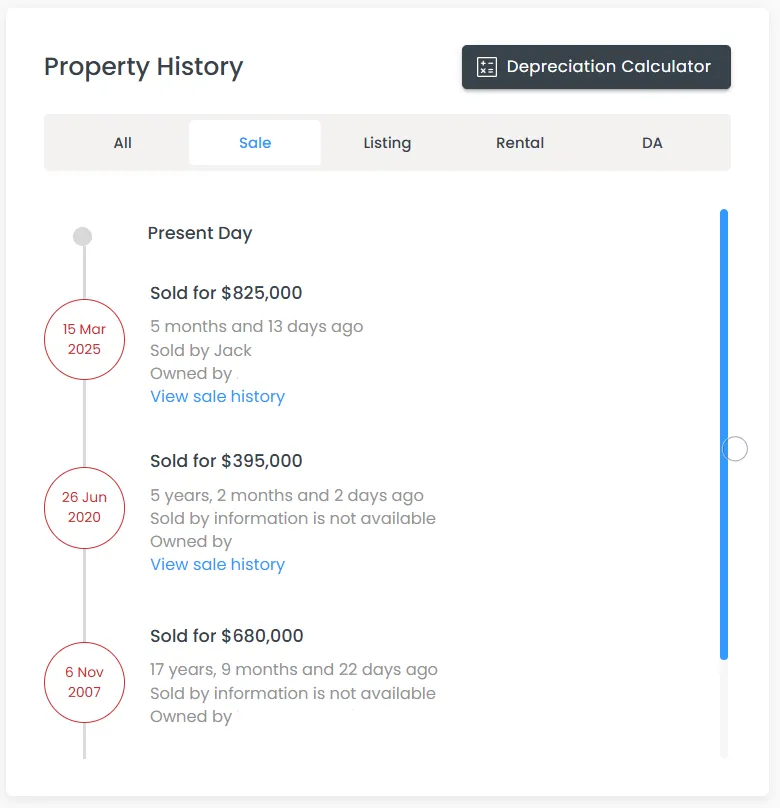

March 15, 2025: $825,000

June 26, 2020: $395,000

November 6, 2007: $680,000

Same property. Same street. Same four walls.

Three completely different financial outcomes.

And here's what nobody wants to admit: the difference had almost nothing to do with the property itself.

It had everything to do with when each person moved—and whether they could survive what came next.

I've Seen This Pattern Destroy People

A few years ago, a real estate agent called me.

You could hear the desperation in his voice.

Join the #1 Newsletter for Property People.

He'd just invested over a million dollars in what he thought was a sure thing.

Regional location. Solid construction. Everything looked perfect on paper.

Then the market turned.

Now he was offering me his completed million-dollar project for $400,000.

Not because the project was flawed.

Not because he'd made some rookie mistake.

Because he got caught on the wrong side of the cycle—and he couldn't hold on long enough to be right.

That phone call wasn't unique. I've watched this pattern play out over and over again.

The carpenter who used to run a successful development company, now back swinging hammers because he over-leveraged at the wrong time.

The developer who built his empire during the boom, only to watch it crumble when the cycle turned.

Same story. Different decade. Different people.

And those three prices at the top? That's the exact same pattern—just playing out on a single asset over 18 years.

This Isn't Theory. This Is What Actually Happens.

Look at those numbers again.

The 2007 buyer paid $680,000. Probably felt smart doing it. Market was strong.

Everyone was buying. Confidence was high.

They held for over 12 years.

And sold for $395,000.

They didn't just miss out on gains.

They lost $285,000.

The exact same asset that just sold in 2025 for $825,000.

So what changed?

Not the property.

Not the location.

Not the fundamentals.

The timing. And whether they could survive what came after.

Here's Where Most People Become Vulnerable

In rising markets, decisions that feel completely rational become traps:

"Sure, it's costing me $400 a week... but it went up $80k this year."

"Negative gearing isn't ideal, but the growth more than covers it."

"Next year it'll be worth even more anyway."

And during the growth phase? They're absolutely right.

If a property rises $100k while costing you $10k a year to hold, the math works.

You're winning.

So that logic becomes your operating system.

And that's exactly when you become exposed.

Because that logic only works in ONE environment.

It requires two things to remain true:

Capital growth continues

You can comfortably hold the asset

If either one breaks, your position weakens.

If both break—and they often do at the same time—you're in serious danger.

What Happens When The Cycle Turns

Markets don't move in straight lines.

At some point—usually when you least expect it—things shift:

Growth slows

Then stalls

Then, in some segments, reverses

Meanwhile:

Interest rates rise or stay elevated

Your holding costs don't care about market sentiment

Rental growth can't keep pace

Now the equation completely flips:

Instead of +$100k growth vs –$10k cashflow , you're facing:

Flat or falling value

Ongoing negative cashflow

No relief in sight

You're bleeding on both sides.

And time—which everyone says is your friend in property—suddenly feels like your enemy.

The Part Nobody Talks About: The Middle

Everyone loves discussing:

The boom (when everyone's making money)

The recovery (when the patient investors get rewarded)

Nobody talks about the middle.

The middle is where you're:

Watching your property do nothing for years

Writing checks every single month

Questioning whether you made a catastrophic mistake

Wondering how much longer you can sustain this

This is where decisions unravel.

Not at the peak.

Not during the crash.

In the long, grinding middle—where doubt turns into pressure, and pressure forces your hand.

How The 2007 Buyer Became The 2020 Seller

They didn't make a reckless decision.

They bought in a strong market. Like most people do.

But then came:

Years of flat or negative performance

Zero equity growth

Relentless holding costs

Mounting financial and emotional pressure

Eventually, the question shifted from:

"Is this a good investment?"

to:

"How much longer can I afford to carry this?"

And that's when the thinking changes:

"Maybe we should cut our losses and move on."

"This isn't performing like we thought it would."

"Let's just sell and redeploy the capital."

And that's how you sell at exactly the wrong time.

Not because you're irrational.

Because the structure of your decision couldn't withstand the cycle.

"It'll Come Back Eventually" — True, But Incomplete

Yes, property tends to recover over time.

Yes, given enough runway, quality assets typically:

Recover losses

Surpass previous highs

Benefit from inflation and supply constraints

But here's the only question that actually matters:

Can you hold long enough for that recovery to happen?

Because life doesn't pause while you wait for the market to save you.

Interest rates change.

Your income changes.

Family situations change.

Your tolerance for ongoing losses changes.

Time can fix the price.

It doesn't eliminate the pressure.

And when that pressure becomes unbearable, you sell—regardless of where the market is.

The Real Risk Isn't The Asset. It's Your Position.

Negative cashflow isn't inherently dangerous.

But it becomes lethal when it's:

Uncontrolled (no buffers, no backup plan)

Poorly timed (late in a cycle when growth is slowing)

Emotionally justified (based on recent performance, not future reality)

In a rising market, negative cashflow feels manageable because growth masks it.

In a flat or falling market, that same cashflow position becomes a financial anchor dragging you down.

The Trap (And Why It's So Common)

Here's the pattern I've watched play out hundreds of times:

Buy in a strong market

Accept negative cashflow because "growth justifies it"

Market slows or stalls

Continue funding the shortfall (what else can you do?)

Fatigue sets in

Pressure mounts

Sell under duress at the worst possible time

Not because the asset was fundamentally flawed.

Because the investor couldn't hold long enough to be proven right.

That agent who called me? That's exactly what happened to him.

The carpenter I worked with years ago who went from running a development company to swinging hammers? Same story.

Different people. Different properties. Same outcome.

What The 2020 Buyer Understood / or was just lucky

The person who bought that property in 2020 entered when:

Confidence was low

Competition was weak

Prices had corrected

Nobody was rushing to buy

It didn't feel exciting. It felt uncertain.

But they had one massive advantage:

They bought at a lower base with capacity to hold.

Five years later, they sold for $825,000.

The exact same property the 2007 buyer lost nearly $300,000 on.

The difference wasn't the asset.

It was timing and position.

The Questions You Need To Be Asking

Before you commit to any property, ask yourself:

Can I comfortably hold this for 10 years if the market goes sideways?

What happens if interest rates stay elevated or rise further?

How much does this cost me every month in a flat market?

Do I have real buffers, or am I banking on growth to bail me out?

If you can't answer those questions clearly and honestly, the risk isn't the market.

It's your position.

Here's What Most People Misunderstand About Cycles

You don't need to perfectly time the market.

But you absolutely need to respect where you are in it.

Because buying well isn't enough.

You need to buy in a way that allows you to stay in the game long enough for time to work in your favor.

The 2007 buyer couldn't.

The 2020 buyer could.

Same property. Completely different outcome.

The Bottom Line

Over the years, I've seen both sides.

I've watched skilled operators lose everything because they ignored timing.

And I've watched smart investors build serious wealth by respecting the cycle and positioning themselves to survive it.

The difference is never the property.

It's whether you can hold long enough to be right.

Those three prices prove it.

That desperate phone call from the agent proved it.

The carpenter who lost his development company proved it.

The pattern repeats. The only question is: which side will you be on?

Want to know where we are in the cycle right now—and what that means for your next move?

That's exactly what The Opportunity Report delivers.

Real insight. No hype. Just the truth about timing, risk, and opportunity—from people who've been in the room when fortunes were made and lost.

CUSTOMER CARE

LEGAL

FOLLOW US

Copyright THE OPPORTUNITY REPORT 2026. All Rights Reserved.